|

|

Every year 4-H Saskatchewan helps to shape the future of more than 3,000 youth members who participate in more than 50 different 4-H projects throughout the province. The 4-H program encourages these members to become engaged in their communities and helps to develop the leadership and life skills necessary for them to become successful and contributing future leaders. This is all made possible because of the generosity and support of those who continue to believe in the 4-H program and continue to invest in the future of our youth. |

Saskatchewan 4-H Foundation Policies

The Saskatchewan 4-H Foundation Gift Planning team is available to work with you and your client to arrange a gift that will best suit your client's charitable and financial needs.

We are professional gift planners who follow the Saskatchewan 4-H Foundation fundraising policies and procedures, Canada Revenue Agency (CRA) regulations, and Canadian Association of Gift Planners (CAGP-ACPDPTM) ethical principles and standards. Any information shared by you or your client will be treated with the utmost discretion and respect.

We are professional gift planners who follow the Saskatchewan 4-H Foundation fundraising policies and procedures, Canada Revenue Agency (CRA) regulations, and Canadian Association of Gift Planners (CAGP-ACPDPTM) ethical principles and standards. Any information shared by you or your client will be treated with the utmost discretion and respect.

Gift Acceptance Policy

Purpose

To ensure that the Saskatchewan 4-H Foundation, as a registered charitable organization, accepts donations/gifts based on informed decisions, that such gifts are receipted in accordance with the Canada Revenue Agency (CRA) regulations and guidelines, and that the donor's intent is adequately documented and appropriately approved.

Principles

This policy is founded on ethical gift acceptance methodologies which are in place to further enhance the mission of the Foundation by aligning with priorities while not hindering its reputation. The Foundation embraces a donor centered philosophy which includes aligning the gift with the original donor intention.

Scope of This Policy

This Policy applies to all gifts accepted by the Saskatchewan 4-H Foundation.

Policy

All gifts must be compliant with Canada Revenue Agency (CRA) regulations and other applicable agency guidelines. Gifts may not be accepted if the donor places parameters on the gift which do not meet Saskatchewan 4-H Foundation policy or fit with Foundation priorities. Ownership of all gifts directed to the Foundation vest in the Foundation. The final decision to accept or decline a gift rests with the Board of Directors. The 4-H Saskatchewan office is responsible for coordinating fundraising, gift acceptance, and gift processing. All gifts to the Saskatchewan 4-H Foundation (cash, gift-in-kind, estate, stock, planned gift) must be processed through the 4-H Saskatchewan office. Financial Services, the primary unit responsible for financial management, is consulted in the gift acceptance process.

Gifts to the Saskatchewan 4-H Foundation that are deemed acceptable will be acknowledged with a charitable receipt as directed by Canada Revenue Agency regulations, and will be used by the Foundation in accordance with the direction, if any, of the donor.

Responsibilities

4-H Saskatchewan office is responsible for coordinating fundraising, gift acceptance, and gift processing. All gifts to the Saskatchewan 4-H Foundation (cash, gift-in-kind, estate, stock, planned gift) must be processed through the 4-H Saskatchewan office. Financial Services, the primary unit responsible for account management, is consulted when necessary, in the gift acceptance process.

Non-Compliance

The Saskatchewan 4-H Foundation expects that its faculty, staff, and agents will comply with this policy. Should there be reason to suspect that laws or Foundation policies have been or are being violated, and the Foundation may suffer reputational, financial or other harm as a result of non-compliance, this may constitute grounds for disciplinary or legal action in accordance with any applicable agreements, contracts, collective agreements, regulations or policies, legislation or common law principles.

Procedures

The 4-H Saskatchewan office will ensure that gifts are given appropriate consideration which includes the creation of trust agreements, receiving endowed gifts, non-cash gifts and financial arrangements.

To ensure that the Saskatchewan 4-H Foundation, as a registered charitable organization, accepts donations/gifts based on informed decisions, that such gifts are receipted in accordance with the Canada Revenue Agency (CRA) regulations and guidelines, and that the donor's intent is adequately documented and appropriately approved.

Principles

This policy is founded on ethical gift acceptance methodologies which are in place to further enhance the mission of the Foundation by aligning with priorities while not hindering its reputation. The Foundation embraces a donor centered philosophy which includes aligning the gift with the original donor intention.

Scope of This Policy

This Policy applies to all gifts accepted by the Saskatchewan 4-H Foundation.

Policy

All gifts must be compliant with Canada Revenue Agency (CRA) regulations and other applicable agency guidelines. Gifts may not be accepted if the donor places parameters on the gift which do not meet Saskatchewan 4-H Foundation policy or fit with Foundation priorities. Ownership of all gifts directed to the Foundation vest in the Foundation. The final decision to accept or decline a gift rests with the Board of Directors. The 4-H Saskatchewan office is responsible for coordinating fundraising, gift acceptance, and gift processing. All gifts to the Saskatchewan 4-H Foundation (cash, gift-in-kind, estate, stock, planned gift) must be processed through the 4-H Saskatchewan office. Financial Services, the primary unit responsible for financial management, is consulted in the gift acceptance process.

Gifts to the Saskatchewan 4-H Foundation that are deemed acceptable will be acknowledged with a charitable receipt as directed by Canada Revenue Agency regulations, and will be used by the Foundation in accordance with the direction, if any, of the donor.

Responsibilities

4-H Saskatchewan office is responsible for coordinating fundraising, gift acceptance, and gift processing. All gifts to the Saskatchewan 4-H Foundation (cash, gift-in-kind, estate, stock, planned gift) must be processed through the 4-H Saskatchewan office. Financial Services, the primary unit responsible for account management, is consulted when necessary, in the gift acceptance process.

Non-Compliance

The Saskatchewan 4-H Foundation expects that its faculty, staff, and agents will comply with this policy. Should there be reason to suspect that laws or Foundation policies have been or are being violated, and the Foundation may suffer reputational, financial or other harm as a result of non-compliance, this may constitute grounds for disciplinary or legal action in accordance with any applicable agreements, contracts, collective agreements, regulations or policies, legislation or common law principles.

Procedures

The 4-H Saskatchewan office will ensure that gifts are given appropriate consideration which includes the creation of trust agreements, receiving endowed gifts, non-cash gifts and financial arrangements.

Investment Policy

Purpose

The Saskatchewan 4-H Foundation uses investments to generate return on assets to fulfill strategies that are aligned with its mission, vision and values. This policy establishes a framework for the investment of funds for the Foundation. This policy:

Principles

The 4-H Saskatchewan mission, vision, and values inspire all of the principles and responsibilities in this policy. The policy was also developed with the following additional principles in mind:

Scope of This Policy

This policy applies to the Foundation's trust and endowment funds, pension assets, pooled cash balance and externally directed agreements. In instances where pension legislation and fiduciary requirements do not align with the policy, pension legislation and governance would supersede the policy.

Policy

Authority over investments is delegated by the Board of Directors and to the Executive Director.

The Foundation's invested funds have the primary objectives to:

The Foundation will not:

Responsibilities

Board of Directors

The Board of Directors maintains accountability for investments through this policy and monitors compliance, investment performance, and investment strategies through reporting from the Executive Director.

Executive Director

The Executive Director is responsible for:

The Saskatchewan 4-H Foundation uses investments to generate return on assets to fulfill strategies that are aligned with its mission, vision and values. This policy establishes a framework for the investment of funds for the Foundation. This policy:

- Establishes the investment objectives and principles for the Foundation's cash and investment assets.

- Defines and assigns the responsibilities of all involved parties.

Principles

The 4-H Saskatchewan mission, vision, and values inspire all of the principles and responsibilities in this policy. The policy was also developed with the following additional principles in mind:

- Risk Management. The risk tolerance of the funds will align with the Foundation's risk management framework. Under the leadership of the Board of Directors and Executive Director, investment risk will be monitored and the following key risk management strategies will be used:

- Consideration of derivatives and other risk management tools to mitigate foreign currency and interest rate risks.

- The level of holdings of particular assets and the quality of certain types of investments will be used to manage credit risk.

- Diversification of asset classes to mitigate market risk and facilitate liquidity requirements.

- Responsible Investing. The Foundation participates in responsible investing by integrating environmental, social and governance (ESG) criteria into the management of the funds. The Foundation believes that, through engagement rather than divestment, the Foundation can play an important role in supporting change and that ESG factors have the potential to affect long-term investment performance.

Scope of This Policy

This policy applies to the Foundation's trust and endowment funds, pension assets, pooled cash balance and externally directed agreements. In instances where pension legislation and fiduciary requirements do not align with the policy, pension legislation and governance would supersede the policy.

Policy

Authority over investments is delegated by the Board of Directors and to the Executive Director.

The Foundation's invested funds have the primary objectives to:

- Fulfill the 4-H Saskatchewan mission and vision in accordance with its values.

- Balance maximization of returns against risks within the scope of the policy.

- Maintain and grow funds for which the Foundation has a fiduciary responsibility.

The Foundation will not:

- Accept and administer funds not in line with the Policy and associated Foundation investment strategies.

Responsibilities

Board of Directors

The Board of Directors maintains accountability for investments through this policy and monitors compliance, investment performance, and investment strategies through reporting from the Executive Director.

Executive Director

The Executive Director is responsible for:

- Establishing structures and strategies to invest the Foundation's resources in alignment with the 4-H Saskatchewan's mission, vision, values, strategic plans, and fiduciary responsibilities.

- Administering the Foundation's investments, including making shifts in investment strategy to align with the Foundation strategy as needed.

- Reporting to the Board of Directors on strategies, performance, compliance, and risk.

Gift Acceptance Guidelines

Click: Gift Acceptance Guidelines to access the Saskatchewan 4-H Foundation guidelines.

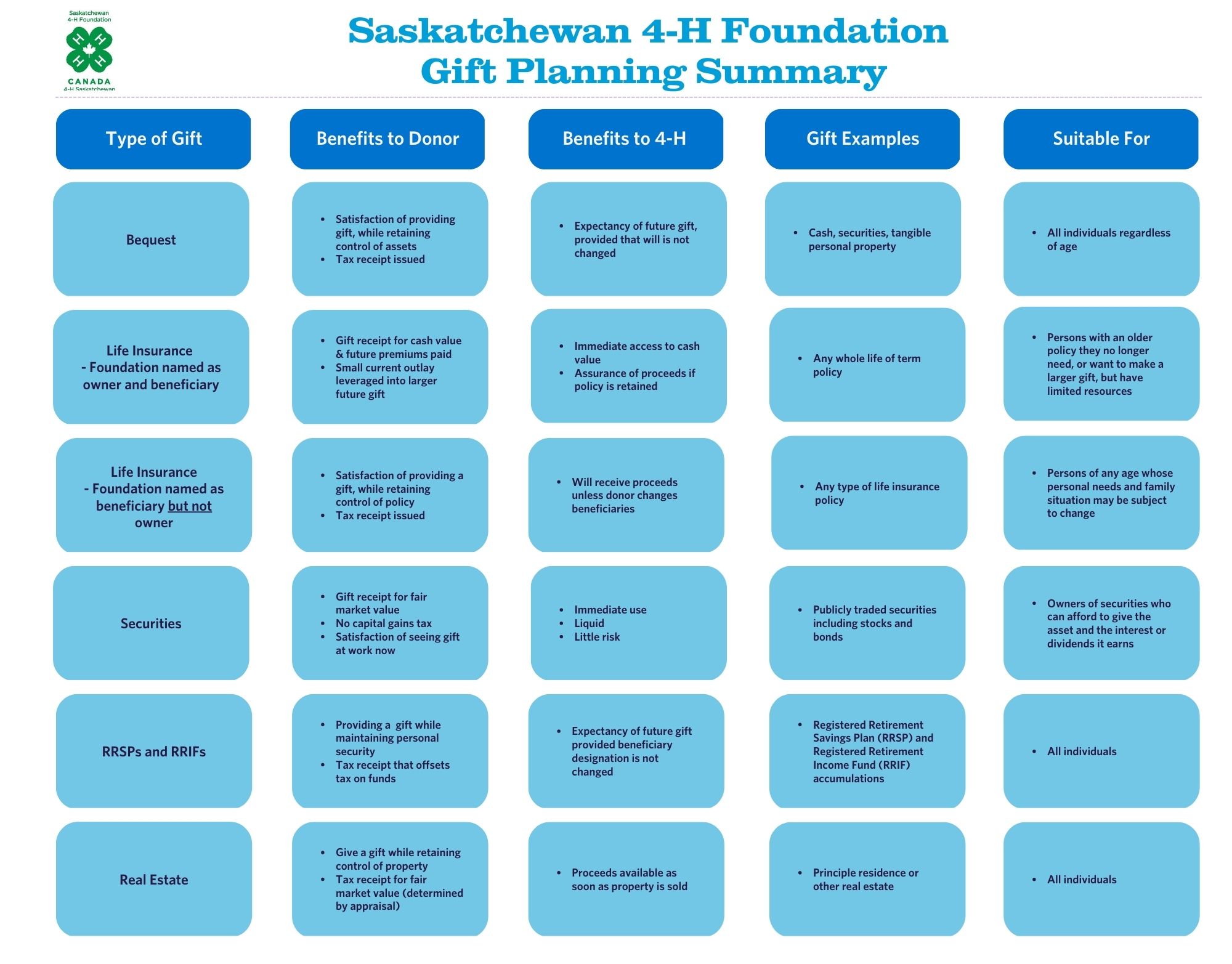

Gift Planning Summary

Click: Gift Planning Summary to access the Saskatchewan 4-H Foundation summary.

Examples of Giving

Bequests

A charitable bequest results in a tax receipt that can be used to offset taxes owing on up to 100% of the donor's taxable income on the final tax return.

Example:

Mr. Harold Bunny leaves a $100,000 bequest in his will to the Saskatchewan 4-H Foundation. Upon his death, his executor transfers cash in this amount to the Foundation. Mr. Harold Bunny's net income reportable on his final tax return is $300,000. His income in the year prior to death was $50,000.

Bequest amount = $100,000

Tax credit (assuming 44% tax rate) = $44,000

Amount claimed on final return = $100,000 (maximum creditable is 100% of net income = $300,000)

Note: The information provided here is for illustrative purposes only and should not be taken as a substitute for professional advice.

- Any amount of the tax credit not usable on the final tax return can be carried back one year to claim a refund on up to 100% of the tax paid in the previous year.

- For receipting purposes, subsection 118.1(5) of the Income Tax Act (Canada) deems a gift made via a Will to be made immediately before the individual has died. The subsequent value of that gift is the value on the date of death, not the value when received by the charity.

Example:

Mr. Harold Bunny leaves a $100,000 bequest in his will to the Saskatchewan 4-H Foundation. Upon his death, his executor transfers cash in this amount to the Foundation. Mr. Harold Bunny's net income reportable on his final tax return is $300,000. His income in the year prior to death was $50,000.

Bequest amount = $100,000

Tax credit (assuming 44% tax rate) = $44,000

Amount claimed on final return = $100,000 (maximum creditable is 100% of net income = $300,000)

Note: The information provided here is for illustrative purposes only and should not be taken as a substitute for professional advice.

Life Insurance

If charity is designated owner and beneficiary:

In the case of a donation of an existing policy with equity, the excess of cash value over the adjusted cost base of policy is taxable to donor at the full income rate and not the capital gains rate.

Example:

Mr. Harold Bunny would like to contribute to the Saskatchewan 4-H Foundation in a substantial way, but he does not have current assets to do so now. He decides to purchase a life insurance policy naming the Saskatchewan 4-H Foundation as owner and beneficiary. The policy is for $100,000 and he makes yearly premium payments of $1,800. The policy will be paid up after 10 years.*

Total premiums paid = $18,000

Donation receipts total = $18,000

Total tax credit (assuming 44% tax rate) = $7,920

After tax cost of policy = $18,000 - $7,920 = $10,080

Thus Mr. Harold Bunny had provided a future gift of $100,000 at a net cost of $10,080.

*A policy that will be paid up over a set period of time was used for illustration purposes. Please note that this type of policy is not always available.

Note: The information provided here is for illustrative purposes only and should not be taken as a substitute for professional advice.

- Tax credit for value of policy and for any premiums the donor continues to pay annually.

- Amount of contribution creditable in any one year is 75% of income. Carry-over period for excess contributions is five years.

In the case of a donation of an existing policy with equity, the excess of cash value over the adjusted cost base of policy is taxable to donor at the full income rate and not the capital gains rate.

Example:

Mr. Harold Bunny would like to contribute to the Saskatchewan 4-H Foundation in a substantial way, but he does not have current assets to do so now. He decides to purchase a life insurance policy naming the Saskatchewan 4-H Foundation as owner and beneficiary. The policy is for $100,000 and he makes yearly premium payments of $1,800. The policy will be paid up after 10 years.*

Total premiums paid = $18,000

Donation receipts total = $18,000

Total tax credit (assuming 44% tax rate) = $7,920

After tax cost of policy = $18,000 - $7,920 = $10,080

Thus Mr. Harold Bunny had provided a future gift of $100,000 at a net cost of $10,080.

*A policy that will be paid up over a set period of time was used for illustration purposes. Please note that this type of policy is not always available.

Note: The information provided here is for illustrative purposes only and should not be taken as a substitute for professional advice.

RRSPs and RRIFs

- If the beneficiary is other than a surviving spouse or dependent(s), the value of the RRSP or RRIF will be taxed as ordinary income, often at the highest marginal rate in the year of death. Hence, it is one of the most heavily taxes estate assets to pass on to children.

- Gifts made by naming Saskatchewan 4-H Foundation as beneficiary (either partial or 100%) on the plan documents.

- Tax credit on donor's final income tax return based on amount contributed from the plan (part or all of assets).

- Amount of gift creditable on final tax return is 100% of income.

- One year carryback, also subject to 100% contribution limit

- Not subject to probate

Example: RRSP

Mr. Harold Bunny, a widow, designates his RRSP which has $50,000 assets to the Saskatchewan 4-H Foundation. He passes away at age 60.

Gift amount = $50,000

Tax of RRSP proceeds (assume 44% tax rate) =22,000

Tax credit =$22,000*

Net tax on RRSP =$0

Thus, the Foundation receives a $50,000 gift, Mr. Harold Bunny's other beneficiaries receive a $22,000 credit that results in no tax being paid on the wind-up of the RRSP.

If the gift was not made, the other beneficiaries would have received a net bequest of $28,000.

* Total tax receipt = $50,000. $22,000 offsets RRSP taxes and can also claim credit against up to 100% of net income on terminal return (with one year carryback).

Note: The information provided here is for illustrative purposes only and should not be taken as a substitute for professional advice.

Securities

- Tax receipt based on fair market value on the day ownership is transferred.

- No capital gains tax on disposition of securities if transferred directly to the university.

- Amount of contribution creditable in any one year is 75% of net income. Carry-over period for excess contributions is five years.

Example:

Mr. Harold Bunny donates 1000 publicly traded shares valued at $10 per share. The shares were $4 per share when Mr. Harold Bunny bought them.

Donation receipt = $10,000

Tax credit (assume 44% tax rate)= $4,400

Capital gain = $10,000 - $4,000 =$6,000

Tax on gain =$0 (since they have been donated)

Net cost of gift = $10,000 - $4,400 = $5,600

If the shares were sold first and the proceeds donated:

Capital gain = $6,000

Taxable gain = 50% X $6,000 = $3,000

Tax on gain (assuming 44% tax rate) = 44% X $3,000 = $1,320

Net tax savings = $4,500 - $1,320 = $3,180

Net cost of gift = $10,000 - $3,180 = $6,850

Therefore, a tax savings of $1,250 will be realized if the shares are donated directly to the Foundation instead of selling them and giving the proceeds to the Foundation.

Information Required to Initiate a Transfer

Saskatchewan Community Foundation:

Krys Hertzke

101-308 4th Ave N

Saskatoon, SK S7K 2L7

(306) 665-1754

RBC Dominion Securities Inc:

Craig Delveaux

301-1074 103A Street SW

Edmonton, AB T6W 2P6

(780) 944-8700

Note: The information provided here is for illustrative purposes only and should not be taken as a substitute for professional advice.

Real Estate

- Tax receipt based on appraised market value.

- 50% of gain taxable to donor.

- Amount of contribution creditable in any one year is 75% of net income. The contribution creditable is increase by 25% of the taxable gain arising from the gift for gifts of appreciated property. The carry-forward period for excess contributions is 5 years.

Example:

Mr. Harold Bunny purchased a rural lot for $40,000 15 years ago and it has recently been appraised for $160,000. He donates the lot to the Saskatchewan 4-H Foundation. The Foundation sells the lot and uses the proceeds.

Donation Receipt issued = $160,000

Tax credit (assuming 44% tax rate) = $160,000 X 44% = $70,400

Capital gain recognized = $160,000 - $40,000 = $120,000

Taxable gain = 50% X $120,000 = $60,000

Tax on gain = 44% X $60,000 = $26,400

Net tax savings = $70,400 (tax credit) -$26,400 (tax on gain) = $44,000 (net savings)

Net proceeds if real estate had been sold* =

$160,000 (selling price) -$26,400 (tax on gain) = $133,600 (net proceeds to donate)

Net cost of donating real estate instead of selling first = $133,600 - $44,000 = $89,600

* For illustration purposes, selling costs have been omitted and the selling price is assumed to be equal to appraised value.

Note: The information provided here is for illustrative purposes only and should not be taken as a substitute for professional advice.

Saskatchewan 4-H Foundation Charitable Registration Number: 119140580RR0001

{kind=link}